How to improve your credit score before applying for a loan or credit card

How to improve your credit score before applying for a loan or credit card

How to Improve Your Credit Score Before Applying for a Loan or Credit Card

How to Improve Your Credit Score Before Applying for a Loan or Credit Card

A credit score is a numerical representation of an individual's creditworthiness, based on their past borrowing and repayment history. It plays a crucial role in determining the interest rates and terms offered on loans and credit cards. A higher credit score typically translates into more favorable loan terms, such as lower interest rates and higher credit limits. Consequently, improving your credit score before applying for a loan or credit card can lead to significant financial benefits.

Understanding the factors that influence your credit score and taking proactive steps to address any negative aspects can significantly impact your borrowing power. A well-maintained credit score can also serve as a measure of financial responsibility, opening doors to other opportunities beyond loan applications, such as securing rental agreements, employment, or even insurance policies.

This article will delve into the intricacies of credit score improvement, providing practical tips and strategies to enhance your creditworthiness and position yourself for favorable financial outcomes.

FAQs about Improving Your Credit Score

Here are answers to some common questions about enhancing your credit score before applying for a loan or credit card:

Question 1: What are the key factors that affect my credit score?

Your credit score is influenced by five main factors: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit (10%). Each of these factors carries a different weight, with payment history being the most significant.

Question 2: How can I check my credit score?

You can access your credit score through various channels, including credit reporting agencies like Experian, Equifax, and TransUnion. Many financial institutions also offer free credit score monitoring services to their customers.

Question 3: What is a good credit score?

A credit score above 700 is generally considered good, while a score above 800 is considered excellent. However, the specific requirements for loan or credit card applications can vary based on lenders' individual policies.

Question 4: How long does it take to improve my credit score?

Improving your credit score requires consistent effort and takes time. The duration depends on your starting score and the strategies you employ. It's essential to be patient and persistent in your efforts.

Question 5: Can I improve my credit score without using a credit card?

While having a credit card can help build credit history, it's not mandatory. You can improve your score by becoming an authorized user on a responsible credit card holder's account or by taking out other types of credit, such as a secured loan or installment loan.

Question 6: What should I do if I have negative items on my credit report?

If you have negative items, such as late payments or collections, it's crucial to understand the reason behind them. You can dispute inaccurate entries with the credit reporting agencies. If the entries are accurate, explore options like debt consolidation or credit counseling to manage your debt effectively.

In conclusion, understanding the factors that influence your credit score and taking proactive steps to address any negative aspects can significantly improve your borrowing power. By utilizing the strategies outlined in this article, you can position yourself for more favorable financial outcomes and achieve your financial goals.

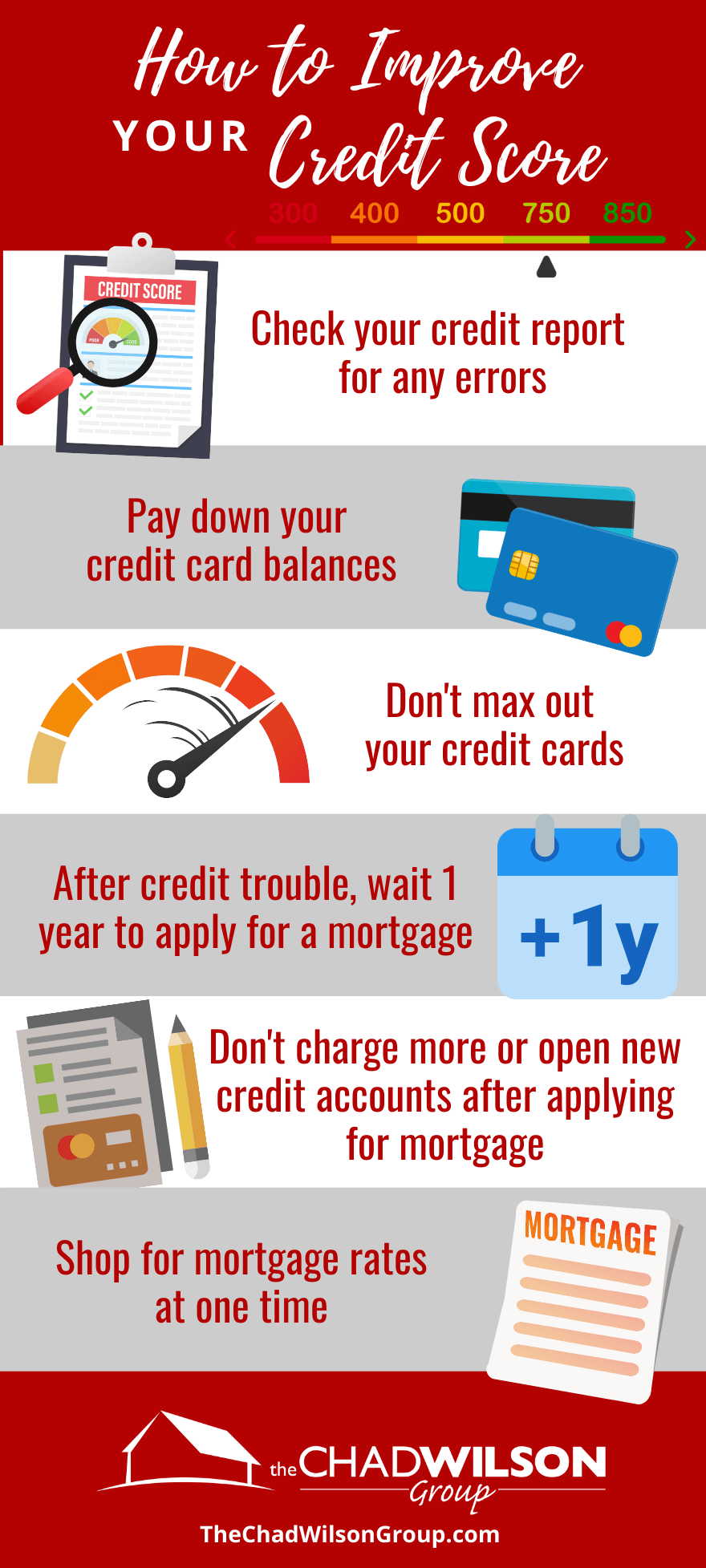

Tips for Improving Your Credit Score

Here are some practical steps you can take to improve your credit score before applying for a loan or credit card:

Tip 1: Make all your payments on time. Punctual payments contribute significantly to your credit score. Set up automatic payments to ensure timely payments and consider using a credit card to manage your spending.

Tip 2: Keep your credit card balances low. High credit utilization ratio, which is the percentage of your available credit you're using, negatively impacts your score. Aim to keep utilization below 30% for optimal results.

Tip 3: Don't apply for too much new credit. Multiple inquiries for new credit can lower your score. Limit your applications to only those that are truly necessary.

Tip 4: Pay down your debt. High debt levels can lower your credit score. Consider strategies like debt consolidation or debt management plans to reduce your outstanding balances.

Tip 5: Become an authorized user on a responsible credit card holder's account. This can help build your credit history and improve your score, even if you don't have a credit card of your own.

Tip 6: Build a diverse credit mix. Having a mix of credit accounts, such as a credit card, a loan, and a mortgage, can positively influence your credit score. However, ensure you manage all accounts responsibly.

Tip 7: Regularly monitor your credit report for errors. Ensure all information is accurate and dispute any inaccuracies with the credit reporting agencies.

Tip 8: Consider using a credit builder loan. These loans are designed to help individuals build their credit history by making regular, on-time payments. While they typically have high interest rates, they can be beneficial for individuals with limited credit history.

Conclusion on Improving Your Credit Score

Improving your credit score requires a multifaceted approach that involves understanding the key factors that influence your score, taking proactive steps to address any negative aspects, and consistently practicing responsible credit management. By diligently making on-time payments, keeping credit utilization low, avoiding excessive applications for new credit, paying down existing debt, and monitoring your credit report, you can significantly enhance your creditworthiness and position yourself for favorable financial outcomes when applying for a loan or credit card.

Remember, a good credit score is a valuable asset that can unlock numerous financial opportunities. By investing in improving your credit score, you are investing in a brighter financial future.

Published on: 2024-10-02T22:10:28.000Z

0 Response to "How to improve your credit score before applying for a loan or credit card"

Post a Comment