Strategies for paying off credit card debt while managing student loans

Strategies for paying off credit card debt while managing student loans

Strategies for Paying Off Credit Card Debt While Managing Student Loans

Strategies for Paying Off Credit Card Debt While Managing Student Loans

Navigating the complexities of student loan repayment while simultaneously tackling credit card debt can be a daunting financial challenge. This situation often arises due to the high costs of education and the temptation of easy credit during the student years. The need to effectively manage both forms of debt is paramount for achieving long-term financial stability.

The benefits of addressing these debts strategically are substantial. Reducing high-interest credit card debt can significantly lower monthly payments, freeing up valuable cash flow. Additionally, a focused approach can improve credit scores, unlocking access to better interest rates on future loans, including mortgages and auto loans. This ultimately contributes to a stronger financial foundation for the future.

This article will delve into various strategies and tips to effectively manage these debts, highlighting the importance of budgeting, prioritizing payments, and exploring potential debt consolidation options.

FAQs about Strategies for Paying Off Credit Card Debt While Managing Student Loans

This section addresses common questions and concerns related to managing both credit card debt and student loans.

Question 1: What is the best approach to prioritize payments between credit card debt and student loans?

Prioritization depends on interest rates and minimum payments. Generally, focusing on credit card debt with higher interest rates is recommended, as it reduces overall interest accumulation faster. However, ensuring minimum student loan payments are met is crucial to avoid default and negative credit implications.

Question 2: Should I consider debt consolidation to simplify my repayment process?

Debt consolidation can be beneficial if it offers a lower interest rate. However, carefully assess the terms, fees, and potential impact on credit scores before consolidating. Consider exploring options for both student loans and credit cards to find the best solution for your specific situation.

Question 3: Are there any government programs available to assist with student loan or credit card debt?

Yes, several government programs exist. The Department of Education offers various options for student loan repayment plans, such as income-driven repayment programs, that tie payments to income levels. Additionally, some credit card companies offer hardship programs to reduce interest rates or defer payments during financial emergencies.

Question 4: What role does budgeting play in managing these debts?

Budgeting is essential for tracking income and expenses. By creating a realistic budget, individuals can identify areas where they can cut spending and allocate more money towards debt repayment. This disciplined approach ensures a focused effort towards financial goals.

Question 5: Can I negotiate with credit card companies to lower interest rates?

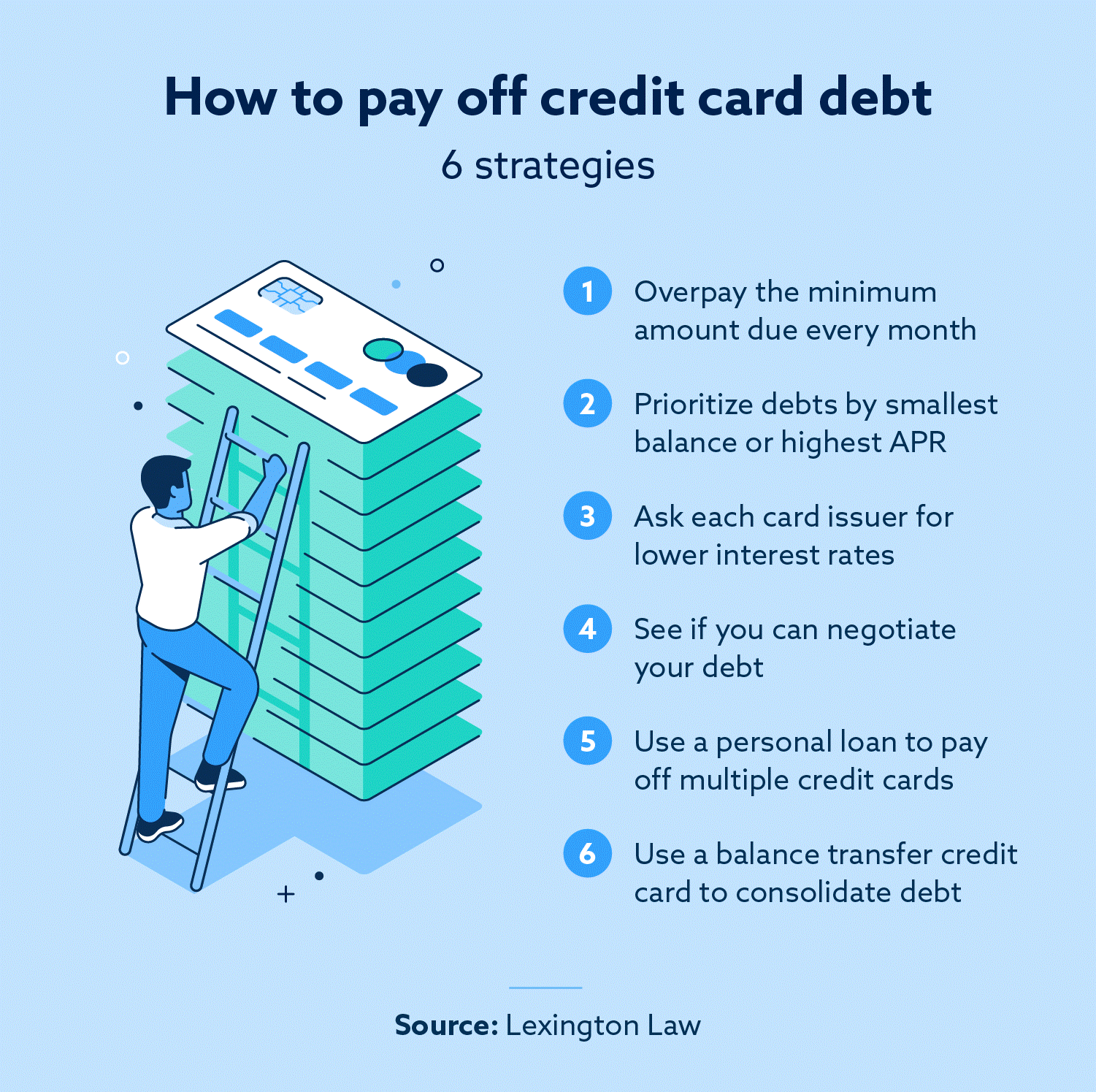

It's worth attempting to negotiate with credit card companies to lower interest rates or fees. A good credit history and consistent payment record can strengthen your negotiation position. Be prepared to present your financial situation and demonstrate your commitment to timely repayment.

Question 6: What is the impact of late payments on my credit score?

Late payments negatively impact credit scores. It's crucial to make payments on time for both credit cards and student loans. Missing payments can lead to increased interest charges, potential collection efforts, and reduced access to future credit.

These FAQs shed light on key considerations and strategies when navigating credit card and student loan debt management. It's crucial to understand your unique circumstances, explore available resources, and make informed decisions to achieve financial well-being.

Tips for Strategies for Paying Off Credit Card Debt While Managing Student Loans

This section provides actionable advice for navigating the complex process of managing both credit card debt and student loan repayments.

Tip 1: Prioritize High-Interest Debt: Begin by tackling credit card debt with the highest interest rates. This approach minimizes overall interest accumulation and allows you to see tangible progress towards debt reduction.

Tip 2: Minimum Payment Plus Extra: Pay the minimum amount due on all debts, but then allocate any extra funds towards the highest-interest credit card. This approach maintains good standing while steadily reducing the most costly debt.

Tip 3: Snowball Method: The snowball method focuses on reducing the smallest debt first, regardless of interest rates. This creates a sense of accomplishment and motivates further debt reduction efforts. After the smallest debt is eliminated, the monthly payment is applied towards the next smallest debt, and so on.

Tip 4: Consider a Debt Consolidation Loan: Explore debt consolidation options, particularly if you have multiple high-interest debts. A consolidation loan can streamline repayment with a lower interest rate, but be sure to assess the terms and fees carefully.

Tip 5: Income-Driven Repayment Plans: For student loans, consider income-driven repayment plans that adjust your monthly payments based on your income level. This can be beneficial if your current income is lower than your anticipated future income. However, these plans may extend the repayment period and increase total interest paid over time.

Tip 6: Budgeting and Spending Control: Creating and adhering to a budget is essential for managing debt effectively. Identify areas where you can reduce unnecessary spending and redirect those funds towards debt repayment. This disciplined approach fosters a path towards financial stability.

Tip 7: Seek Professional Advice: Don't hesitate to seek professional financial advice from a certified financial planner. A qualified planner can provide personalized guidance based on your individual financial situation and goals.

These tips offer practical strategies for effectively managing credit card debt while simultaneously handling student loan obligations. Remember, a combination of disciplined budgeting, focused repayment, and careful consideration of available resources can lead to a more secure financial future.

Conclusion on Strategies for Paying Off Credit Card Debt While Managing Student Loans

This article has explored a multifaceted approach to managing credit card and student loan debt simultaneously. It's essential to prioritize high-interest debt, employ various payment strategies like the snowball method, and explore options for consolidation or income-driven repayment plans. Budgeting and spending control play a vital role in achieving financial stability and achieving your debt reduction goals.

Taking proactive steps to manage your debt is crucial for building a strong financial foundation. Remember, seeking professional guidance and understanding your financial situation are key ingredients for navigating this challenging but ultimately rewarding journey towards financial freedom.

Published on: 2024-10-12T17:38:51.000Z

0 Response to "Strategies for paying off credit card debt while managing student loans"

Post a Comment